Securing a car loan with bad credit in Canada may seem like an uphill battle, but it’s far from impossible. Whether you’ve faced bankruptcy, missed payments, or simply have a limited credit history, there are lenders across the country who specialize in helping people rebuild their financial lives with reliable transportation.

Limited Time Automotive Amazon DealsIn this in-depth guide, we’ll walk through how bad credit affects your chances of getting approved, how subprime lenders work, tips for improving your approval odds, and what to watch out for during the process.

Understanding Bad Credit

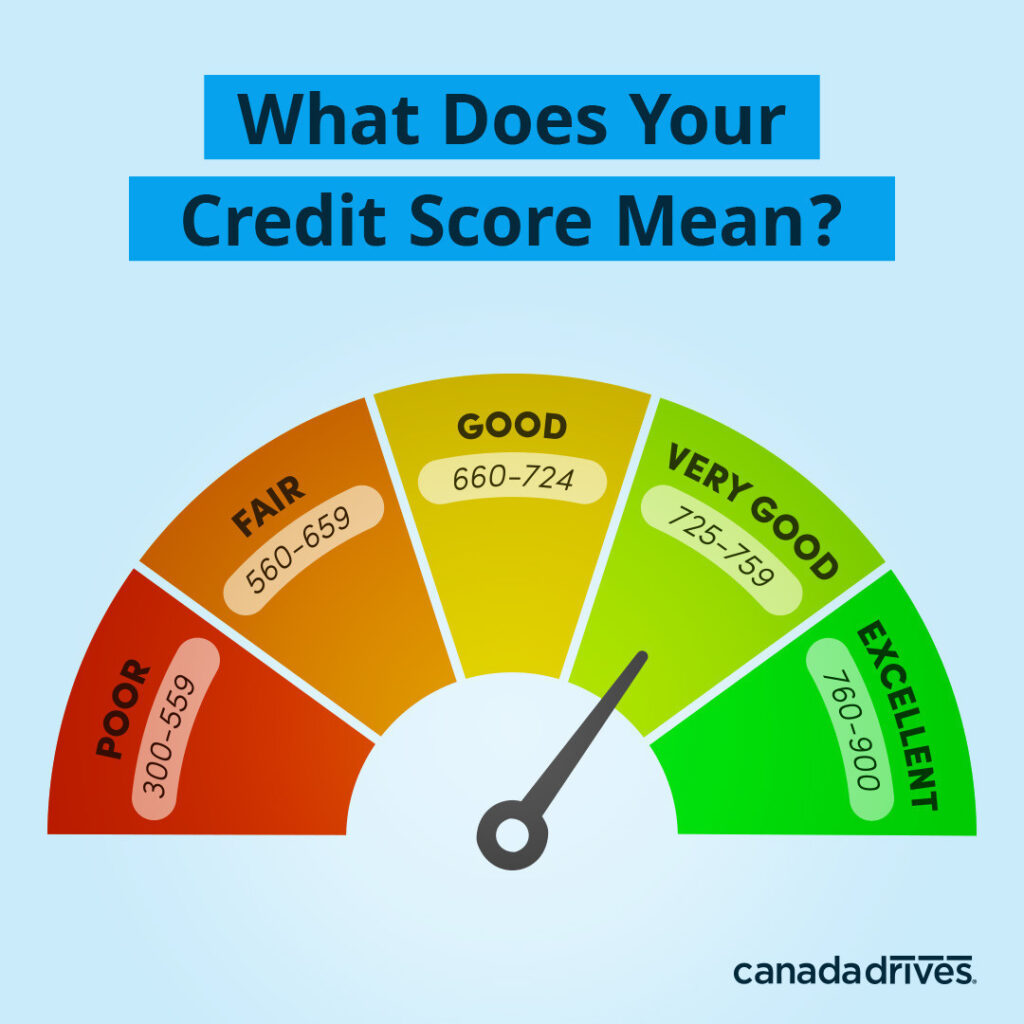

Your credit score is a reflection of your financial history—mainly how well you’ve managed credit in the past. In Canada, credit scores typically range from 300 to 900. Here’s a basic breakdown:

| Credit Score Range | Rating | Loan Approval Likelihood |

|---|---|---|

| 760 – 900 | Excellent | Very High |

| 725 – 759 | Good | High |

| 660 – 724 | Fair | Moderate |

| 560 – 659 | Poor | Challenging |

| Below 560 | Very Poor | Difficult but Possible |

If your score is below 660, you’re generally considered a “bad credit” borrower. This doesn’t mean you can’t get approved—it just means you may face higher interest rates or stricter conditions.

Can You Get a Car Loan with Bad Credit?

Yes, you can get a car loan even if your credit score is low. Several lenders and dealerships in Canada specialize in “subprime auto financing,” which means they work specifically with customers who have poor credit, no credit, or a bankruptcy on record.

These lenders consider more than just your credit score, including:

- Current employment and income

- Length of time at your job

- Monthly debt obligations

- Down payment size

- Stability of residence

By focusing on your current ability to repay the loan—not just your past—you stand a much better chance of approval.

Types of Lenders for Bad Credit Car Loans

Here are the main types of lenders offering car loans to people with poor credit:

| Lender Type | Description | Pros | Cons |

|---|---|---|---|

| Bank or Credit Union | Traditional institutions with strict criteria | Trusted, lower interest | Harder to qualify |

| Dealership Financing | Dealerships working with subprime lenders | One-stop shopping | Rates may be higher |

| Online Lenders | Digital platforms specializing in bad credit loans | Fast pre-approval, competitive | Varies by lender reputation |

| Buy Here, Pay Here | Dealer acts as lender, no external financing | No credit checks | Higher rates, fewer protections |

How Much Can You Borrow?

The loan amount you qualify for depends on several variables:

- Your gross monthly income

- Debt-to-income ratio (how much you owe vs. what you earn)

- Vehicle type and age

- Down payment offered

Most bad credit car loans range from $5,000 to $35,000. A typical lender will want to ensure your monthly vehicle payment does not exceed 20%–25% of your gross monthly income.

What Interest Rates Can You Expect?

Interest rates for borrowers with bad credit are higher to offset lender risk. Here’s what you can expect:

| Credit Score Range | Estimated Interest Rate (2025) |

|---|---|

| 700+ | 4.99% – 7.99% |

| 600 – 699 | 8.99% – 14.99% |

| Below 600 | 15.99% – 29.99% |

While a 20% interest rate may seem steep, remember that timely payments on this loan will rebuild your credit, improving your score over time.

Tips to Increase Your Chances of Approval

If you’re applying for a car loan with bad credit, follow these steps to maximize your chances:

1. Check Your Credit Report

Request your free credit report from Equifax or TransUnion. Look for errors and dispute any inaccuracies.

2. Offer a Down Payment

A down payment of even $1,000–$2,000 shows commitment and reduces lender risk. It can also lower your monthly payments.

3. Get a Co-Signer

If someone with good credit is willing to co-sign, it can help you get approved and secure a lower rate.

4. Choose a Budget-Friendly Vehicle

Focus on reliability, fuel efficiency, and low maintenance costs. Avoid luxury models or high-mileage used cars.

5. Shop Around for Lenders

Don’t settle for the first offer. Compare multiple quotes from banks, credit unions, and online lenders.

Rebuilding Your Credit with an Auto Loan

A car loan can be a powerful tool to repair your credit. Here’s how:

- Timely Payments: Each on-time payment improves your credit score.

- Credit Mix: Adding an installment loan (like a car loan) strengthens your credit profile.

- Debt Reduction: Over time, your debt-to-income ratio improves, especially if you avoid credit card debt.

Many borrowers see their credit score improve within 6 to 12 months of responsible auto loan payments.

Red Flags and What to Avoid

When seeking a car loan with bad credit, be cautious of the following:

| Red Flag | Why It Matters |

|---|---|

| No Credit Check Offers | Often tied to high interest or hidden fees |

| Extremely Long Loan Terms | Low monthly payments but huge interest costs |

| No Breakdown of Fees | Transparency is key—demand a full cost summary |

| Pressure to Buy | Walk away from dealers using scare tactics |

Always read the fine print and understand your total cost of borrowing before signing anything.

Where to Apply for Bad Credit Car Loans in Canada (2025)

Here are some trusted lenders and platforms that specialize in bad credit auto loans:

| Company Name | Description | Application Time |

|---|---|---|

| Canada Drives | Online application, nationwide | ~5 minutes |

| Clutch | Online used car buying, financing | ~10 minutes |

| Car Loans Canada | Nationwide lender network | ~5 minutes |

| DriveTime Canada | Focused on poor credit customers | ~10 minutes |

| Local Dealerships | Many offer in-house financing | Varies |

Final Thoughts

Getting a car loan with bad credit in Canada may require extra steps and research, but it is achievable—and potentially life-changing. Reliable transportation can open doors to better jobs, increased freedom, and the ability to rebuild your financial standing.

Take the time to check your credit, budget responsibly, explore multiple options, and work with lenders who are transparent and experienced in bad credit financing. Remember, this is more than just buying a car—it’s an opportunity to get back on track.