It is one of the automotive industry’s best-kept secrets—a financial “backdoor” that can allow you to drive a luxury vehicle for the price of a budget sedan. But unlike leasing a new car, which is as standard as ordering coffee, leasing a used car requires navigating a maze of specific dealerships, Certified Pre-Owned (CPO) programs, and credit requirements.

Limited Time Automotive Amazon DealsIf you are tired of the steepest part of the depreciation curve but don’t want to commit to owning a depreciating asset, this guide is your roadmap.

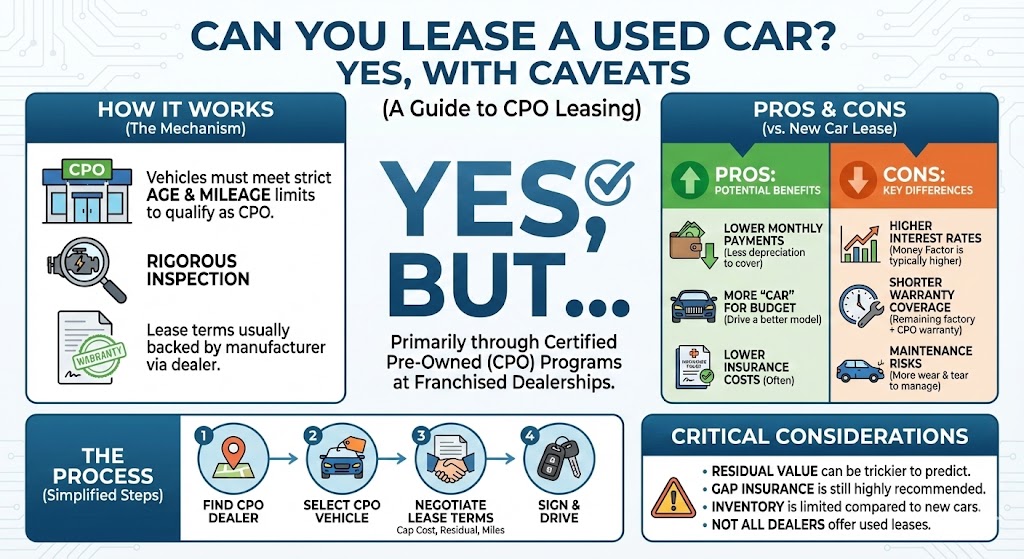

The Cheat Code: Why Lease Used?

The primary appeal of leasing a used car is simple: Depreciation.

Limited Time Automotive Amazon DealsWhen you lease a new car, your monthly payment is essentially covering the difference between the car’s sticker price (Capitalized Cost) and what it will be worth in three years (Residual Value). Since a new car loses up to 20% of its value the moment it drives off the lot, that gap is huge—and you pay for it.

A used car has already taken that massive depreciation hit. The gap between its current price and its future value is much smaller. Theoretically, this leads to significantly lower monthly payments.

The “Sweet Spot” Benefits:

- Luxury for Less: You could potentially drive a 3-year-old BMW 5-Series for the same monthly payment as a brand-new Honda Civic.

- Lower Insurance: Since the car’s replacement value is lower, insurance premiums are often cheaper.

- Shorter Commitments: Used leases can sometimes be found for shorter terms (12–24 months), especially via lease takeovers.

The Three Paths to Leasing Used

You generally cannot walk into any random dealership and ask to lease the 2015 sedan sitting in the back row. Used leasing typically happens through three specific channels.

1. Certified Pre-Owned (CPO) Leasing

The Gold Standard.

Most major manufacturers (specifically luxury brands like BMW, Mercedes-Benz, Lexus, Audi, and Acura) have official CPO leasing programs.

- How it works: You lease a CPO vehicle that is usually less than 4 years old and has low mileage.

- Why it’s safe: These cars undergo rigorous inspections to meet factory standards and, crucially, often come with a warranty that matches the lease term.

- Availability: High. Most franchise dealers can structure a lease on their CPO inventory.

2. Independent Dealer Leasing

The Wild West.

Some independent “used car superstores” or luxury specialty lots offer their own leasing programs.

- How it works: The dealership acts as the bank or partners with third-party leasing companies to write the lease.

- The Risk: These deals often come with higher money factors (interest rates) and less transparent terms. The cars may not be “certified” by a manufacturer, meaning you are on the hook if the engine blows up in month 5.

3. Lease Takeovers (Swap-a-Lease)

The Loophole.

This isn’t starting a new lease; it’s taking over the remaining months of someone else’s.

- How it works: You find a driver desperate to get out of their lease early. You go through a credit check with the leasing company, and the contract is transferred to your name.

- The Benefit: No down payment (usually), and you often get a short term (e.g., 14 months left on a 36-month lease).

- The Trap: You inherit the previous owner’s mileage usage and any hidden wear-and-tear damage.

Deep Dive: The Math of Used Leasing

To understand if this is right for you, you have to look at the equation. A used car lease isn’t always cheaper. Here is the tension between Depreciation and Interest.

| Factor | New Car Lease | Used Car Lease | Winner |

| Depreciation | Massive. You pay for the steepest drop in value. | Minimal. The curve has flattened out. | Used |

| Money Factor (Interest) | Often subsidized (“subvented”) by the factory. Can be near 0%. | usually standard market rates. Can be higher to offset risk. | New |

| Residual Value | High dollar amount, but a low percentage of the start price. | Lower dollar amount, but the gap to bridge is smaller. | Used |

| Maintenance | Zero (Warranty + Free Maintenance plans). | Risky. You may pay for repairs on a car you don’t own. | New |

Critical Warning: If the interest rate (Money Factor) on a used lease is high enough, it can completely erase the savings gained from lower depreciation. Always calculate the total cost of the lease term, not just the monthly payment.

The Pitfalls: What Can Go Wrong

Leasing a used car introduces variables that don’t exist with new cars. If you aren’t careful, these can cost you thousands.

1. The Warranty Gap

This is the single biggest risk.

- Scenario: You lease a 4-year-old car for 3 years.

- Problem: The original factory warranty likely expired at year 4 or 5.

- Nightmare: In year 2 of your lease (the car’s 6th year), the transmission fails. You now have to pay $3,000 to fix a car that you do not own and will have to give back in 12 months.

- Solution: Only lease CPO vehicles where the warranty covers the entire duration of the lease.

2. Residual Value Arguments

With new cars, the residual value is set in stone by the manufacturer. With used cars, the dealer has more wiggle room to manipulate this number. A lower residual value means higher monthly payments for you. You need to ensure the residual value they are using is fair market value.

3. Hidden Wear and Tear

When you return a leased car, you are charged for “excess wear and tear.”

- The Trap: On a used car, there is already wear and tear when you get it.

- The Fix: You must document every scratch, dent, and stain before you drive off the lot. If it isn’t documented, you will be blamed for it when you return the car.

Step-by-Step Guide to Leasing a Used Car

If you are ready to hunt for a deal, follow this protocol.

Step 1: Target the Right Brands

Focus on luxury brands. Budget brands (Honda, Toyota, Ford) often have such high resale values and cheap new-lease deals that leasing them used doesn’t save you enough money to be worth the hassle.

- Best Bets: BMW, Audi, Mercedes-Benz, Acura, Infiniti, Porsche.

Step 2: Find the “Certified” Inventory

Go to the manufacturer’s website (e.g., BMW.ca or Lexus.com) and search their “Certified Pre-Owned” inventory. Do not just look at “Used”—look specifically for “CPO.”

Step 3: Call the Finance Manager Directly

Salespeople on the floor often don’t know how to structure used leases or don’t want to because the commission is lower.

- The Script: “I am looking at Stock #12345, the CPO 2021 X5. Does your dealership offer leasing on CPO units, and if so, what is the current money factor and residual for a 36-month term?”

Step 4: Audit the Warranty

Ask explicitly: “Will the CPO warranty cover the vehicle for the full 36 months of this lease?” If the answer is no, ask for the cost to extend it. Add that cost to your monthly payment calculation.

Step 5: The “New vs. Used” Comparison

Before signing, ask the dealer to quote you a lease on a brand new version of the same model.

- Sometimes, manufacturers offer aggressive incentives (like 0.9% financing) on new cars that make the payment practically the same as the used one. If the difference is less than $50/month, take the new car.

Alternative Route: The Lease Takeover

If dealerships aren’t offering what you want, you can look at the secondary market. Sites like LeaseBusters (Canada) or SwapALease (US) are marketplaces for lease transfers.

Why do this?

- No Down Payment: The original owner already paid the freight/PDI and down payment.

- Incentives: Desperate sellers often offer cash incentives (e.g., “I will give you $2,000 cash to take this car”).

The Checklist for Takeovers:

- Check Mileage: specific calculation. (Current Odometer + (Remaining Months * Monthly Allowance)). Does this match your driving needs?

- Check Condition: You need a professional inspection. Do not trust the seller’s photos.

- Transfer Fees: Who pays the $500–$1,000 transfer fee? (Negotiate this).

Summary: Who Should Do This?

Leasing a used car is PERFECT for you if:

- You want a luxury badge (BMW/Benz) but cannot afford the $900+ new car payment.

- You drive average mileage (10k–12k miles/year).

- You are financially literate enough to calculate the “total cost of lease.”

- You find a CPO car with a warranty that covers the full lease term.

Do NOT lease a used car if:

- You drive high mileage (20k+ miles/year).

- You are looking at economy cars (Civics/Corollas)—just buy them or lease new.

- You have poor credit (Used leases are often stricter on Tier 1 credit).